As we usher in 2025, the air is buzzing with optimism, driven by the enthusiasm that followed Donald Trump’s election and a slim Republican majority in Congress. This excitement has translated into exuberant market forecasts, with predictions of robust economic growth, rising profits, lower taxes, and diminished regulation.

However, unexpected challenges may lie ahead.

The Annual Forecast Ritual

Each year, financial services professionals and economists unveil their forecasts for the coming year. They always include a few standard disclaimers, such as, “There is no assurance that the views or strategies discussed will yield positive outcomes.”

We believe that they should clearly state "unless there are surprises." Surprises are a certainty, as history continually proves (see Investor Sentiment below). Yet, our aversion to uncertainty fuels the need for these predictions. So, the following are excerpts of the forecasts from the independent research firms that we subscribe to.

Argus Research offers an upbeat outlook. They foresee lower interest rates, stable economic growth, and corporate profit increases reaching low double digits. A decline in inflation may nudge the FED to trim short-term rates further. The pivotal factors will be the Fed's decisions and the impact of President Trump's economic policies on inflation and subsequently earnings growth. Historically, the first-year post-election tends to be favorable for equity returns.

Potential Disruptors

As you are aware, significant uncertainties loom. Geopolitical tensions, tariff policies, and President-elect Trump's proposed changes present formidable unknowns. Wolfe Research, another of our independent sources, identifies several potential disruptors:

- Rising long-term interest rates,

- Broader and higher tariffs,

- Underwhelming AI investments,

- Unexpected inflation increases.

These are not predictions but scenarios worth monitoring.

A Closer Look at the Economy

The ISM Manufacturing Index climbed to 49.3 in December, the highest in nine months, nearing the expansion threshold of 50. Concurrently, the Services PMI® stood at 59.3, marking expansion for the 52nd time in 55 months since the post-pandemic recovery began in June 2020.

China's economic trajectory, projected to slow to an average of 3.8% annually over the next fifteen years, remains critical for the US. China's economy, contributing 30% to global growth, is nearly as influential as the combined output of the next four largest economies, including the US.

Global economic growth, according to the International Monetary Fund's October World Economic Outlook, is expected to remain steady yet unremarkable at 3.2% in 2024 and 2025.

Market Dynamics

The S&P 500 has surged by 25% (source: Slick Charts), with the bulk of gains concentrated in the top 10 stocks. This concentration, where only 19% of stocks in the index rose by more than 25%, reflects a market heavily reliant on a few key players.

The MSCI EAFE index, representing non-U.S. companies, sits at 3.29%.

The graph below shows how volatile the rate on 10-year U.S. Treasury bonds has been this past year. The rise from early November through the end of the year caused a general decline in dividend-paying stocks in December.

Who Would Want to Be The Chairman of The FED?

In December 2024, the Fed trimmed its target interest rate by 0.25% to 4.25%- 4.5%. Fed Chairman Jerome Powell signaled a cautious approach, reflecting higher inflation readings and expectations. Most forecasters remain optimistic about reducing inflation to 2%, albeit over the next couple of years. Some of President-elect Trump's proposals could exacerbate inflationary pressures, though this remains speculative.

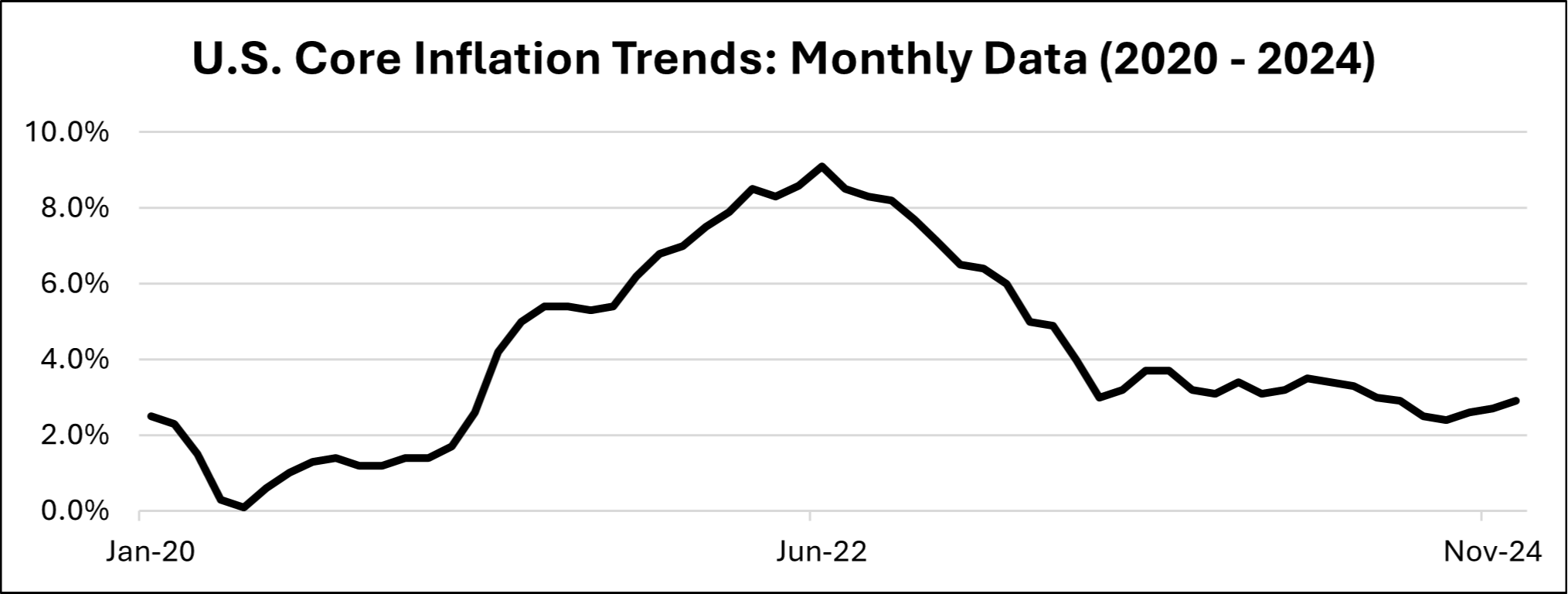

Everybody Talks About Inflation

The rate of inflation for the year was announced on January 15, 2025. In 2024, the U.S. year-over-year inflation rate is 2.97%, a slight uptick from November’s 2.7%, Leading contributors were food prices (including dining out) were up 4.2. Energy costs were up 3.8% due to a hike in December. I suspect this was due to the colder-than-normal temperatures. Healthcare costs up 3.0%. I find it encouraging that the rate of increase in healthcare costs has declined over the past decade. (Source: Peterson-KFF Health System Tracker)

Employment Trends

The U.S. unemployment rate, which stood at 4.2% in November, was 4.1% in December. The number of new jobs created was higher than expected.

Predictable Unpredictability

In Morgan Housel's book "Same as Ever," the focus is on recognizing predictable elements amidst unpredictability. Jeff Bezos, founder of Amazon, is quoted as saying that understanding what won’t change is more crucial than trying to guess what will. Housel posits that human behavior oscillates between greed and fear. Other persistent factors include rising debt, sharply contrasting political-economic views, and progressing deglobalization, which will shape the economy, markets, and international relations.

Investor Sentiment: A Pendulum Swinging

Howard Marks, an investment luminary, uses the pendulum analogy to describe market sentiment. Inspired by his philosophy, I installed a large pendulum clock in my office as a constant reminder. Currently, the pendulum swings towards high confidence.

The Cautionary Tale of Averages

The investment management industry often touts the long-term average annual return of the S&P 500 as around 10%. However, this figure depends on the period selected. Since 1926, annual returns have fallen between eight and 12 percent only six times.

Some Good News

Teenage substance abuse and alcohol consumption are on the decline. Credit card debt relative to disposable income is lower than pre-pandemic levels. While governmental debt is alarming, household debt relative to income and assets has dropped significantly over the past fifteen years.

Final Thought

Peter Bernstein, a legendary investor, once said, "There is a tendency for people to expect the status quo to last indefinitely or to provide advanced signals for shifting strategies. The world doesn't work like that. Surprise and shock are endemic to the system, and people should always arrange their affairs to survive such events, rather than focusing all the time on getting rich." Morgan Housel adds, "A good summary of investing history is that stocks pay a fortune in the long run but seek punitive damages when you demand to be paid sooner."

Written by Bruce Pienton, Managing Partner & Wealth Advisor